By Jon McKinney

Managing Partner & Portfolio Manager

President’s Letter Q4- 2025

“He plays a game with which I am not familiar”

In 1997, a 21-year-old won the Masters by a record 12 strokes. This is arguably the most important golf tournament in the world. He was already a three-time winner of the US Junior Amateur, and had won twice on the PGA in 1996 and once in 1997. The player is of course Tiger Woods, and his win was nothing short of epic. He was the youngest winner ever, his score of 18 under was a Masters record and he was the first black golfer to win. The victory was a cultural milestone that prompted millions of non-golf fans to pay attention to golf. Golf would never be the same.

Legendary golfer and co-founder of the Masters, Bobby Jones, once said of Jack Nicklaus: “He plays a game with which I am not familiar”. After Tiger’s 1997 Master’s win, Jack copied Jones’ famous quote saying of Tiger: “He’s certainly playing a game we’re not familiar with”. Tiger had taken the game of golf to a new level.

So, what did the world’s best golfer do after his Masters win? He changed his swing!

Woods and his coach at the time, Butch Harmon, analyzed his swing and they saw elements that could be exposed under pressure. Tiger made the changes not to win by even more, but to create a more reliable, repeatable swing that would produce a smaller margin of error on his bad shots. It would allow him to compete even when his swing was not “in the zone”.

Quintessence Wealth

How does a golf story relate to the world of investment management? This may be a bit of a stretch, but when we look at our performance over the past 5 years, we feel pretty good about “our swing” and yet we’ve decided we could still improve it. As most of you now know, we are partnering with Quintessence Wealth or Q Wealth, a Canadian-owned national portfolio manager and investment fund manager group that can support us in all areas of customer service, technology, compliance, trading, custodianship and investment offerings. Importantly we remain independent, but we can now harness the resources of the bigger group. It allows us to put all our focus our clients, without the distraction of managing the technical details of a back office.

We believe the changes we are making will improve the service and results we always try to deliver to our clients. We’re excited to partner with Q Wealth and we hope you, our clients, will reap the rewards.

Proactive adaption, long-term vision and significant change

Tiger Woods’ best year is widely considered to be 2000, a season of unparalleled dominance where he won nine PGA Tour events, including three consecutive majors, the U.S. Open by 15 strokes, The Open Championship by eight strokes, and the PGA Championship in a playoff. He finished in the top five in 17 of 20 events and set numerous scoring records. Tiger’s 2000 season is often called the greatest golf season in history.

His next move? He changed his swing again!

When Tiger changed his swing, he was using proactive adaption, long-term vision and using his periods of success as low-risk windows for significant change. We may not be Tiger Woods, but we get it. We see an opportunity to use the power of the Quintessence Wealth partnership to help us better serve our clients.

Please let us know if you have any questions about this new chapter for ZLC Wealth.

Below is a review of the market trends in the forth quarter prepared by Yin Chan, CFA, our Investment Analyst.

Quarterly Market Commentary – Q4 2025

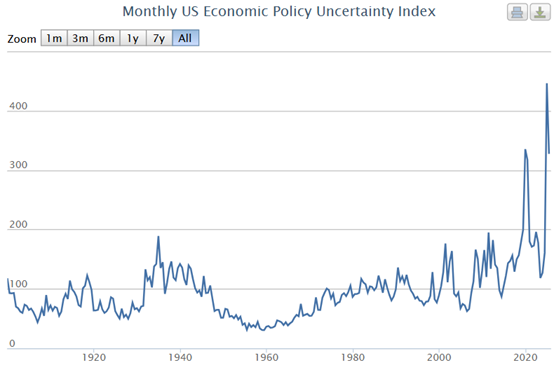

Policy Uncertainty and Political Influence

The Q4 of 2025 marked a significant shift in how markets perceive risk. Earlier in the year, investors focused on inflation coming down and interest rates eventually falling. By the end of the year, the focus changed. Markets began to price not just economic data, but policy uncertainty and political influence more directly.

One of the defining themes late in the quarter was the growing role of policy uncertainty in the United States. Markets started to pay closer attention to the direction of U.S. monetary leadership. President Trump signaled that he plans to name the next Federal Reserve Chair earlier than usual in 2026. This raised questions about the independence of future monetary policy and whether rate decisions could become more politically influenced.

Source: https://www.policyuncertainty.com/

Investors had to consider fresh risks related to US fiscal policy at the same time. The prospect of another government shutdown reappeared, underscoring continued financial strain and political polarization. These risks contributed to a more cautious tone, even though markets did not react sharply. Strong growth assumptions and aggressive rate cuts were no longer as appealing to investors.

Rates on Hold

Although the process remained uneven, inflation continued to approach central bank targets. While core inflation remained marginally higher, headline inflation in Canada stabilized around 2%. The Bank of Canada’s message that inflation is declining but not entirely under control was reaffirmed by this pattern. As a result, central banks shifted toward patience. Rate cuts were no longer viewed as urgent or guaranteed. Instead, they became conditional on further softening of economic data. For investors, this meant adjusting expectations. Lower rates are still possible, but the path is slower and more dependent on incoming data.

Source: https://tradingeconomics.com/canada/inflation-cpi

Policy actions in the U.S. also highlighted how governments are trying to support growth without reigniting inflation. President Trump directed U.S. housing agencies to purchase additional mortgage bonds to lower mortgage rates. This move aimed to support housing affordability and stabilize demand.

Markets were aware of this strategy’s limitations, though. On their own, such measures are unlikely to spur a robust housing recovery, even though they might offer temporary respite. Affordability, supply issues, and cautious lending standards continue to be barriers to housing. This reaffirmed the quarter’s overarching theme, which is that while policy support can reduce downside risk, it cannot compel growth.

Trade policy was another topic that came up again towards the end of the quarter. It was anticipated that the U.S. Supreme Court would rule on tariffs imposed under emergency powers. The result might change or reverse current tariffs, creating more uncertainty for supply chains and companies.

Even without immediate changes, the possibility of rapid policy shifts affected corporate planning and investment decisions. For markets, this reinforced a preference for companies with flexible supply chains, pricing power, and lower exposure to global trade disruptions.

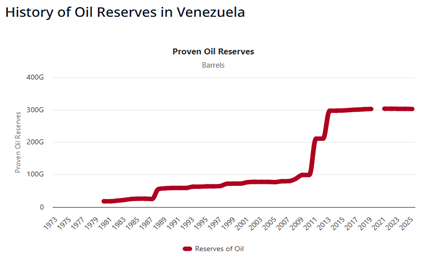

Maduro in Handcuffs

Just after year-end, a significant geopolitical development surfaced. Venezuela’s leadership was overthrown by a U.S. military operation, and the nation was placed under an American-backed transitional framework. This event brought Venezuela’s substantial oil reserves and its long-term contribution to the world’s energy supply back into the spotlight.

Source: https://www.worldometers.info/oil/venezuela-oil/

Investors responded with both curiosity and caution. Although Venezuela offers potential upside in energy supply, political stability remains uncertain, infrastructure is inadequate, and significant investment would be required before production could meaningfully recover. Beyond Venezuela itself, investors also raised broader concerns. The ability of the U.S. to intervene and take control with limited immediate consequences prompted questions about whether similar actions could occur elsewhere. This uncertainty around geopolitical boundaries and enforcement added to market unease.

Chasing returns was not the focus of Q4 2025. It had to do with redefining expectations. Instead of being a shock, inflation became a background problem. Rate reductions were no longer assumed, but rather conditional. In asset pricing, political and policy risk became more apparent. The choice of assets was more important than the general direction of the market.

Considering this, we kept using an all-weather approach to portfolio management. We placed a strong emphasis on diversification across geographical areas and asset classes. To remain adaptable as geopolitical and policy risks change, we also kept liquidity. This approach reflects our view that the current environment rewards discipline more than prediction. Markets can move sideways for long periods. During those periods, balance and consistency matter most.

Sources:

- https://www.policyuncertainty.com/

- https://tradingeconomics.com/canada/inflation-cpi

- https://www.worldometers.info/oil/venezuela-oil/

Disclaimer:

This newsletter is solely the work of the author for the purpose to provide information only. Although the author is a registered Investment as a Portfolio Manager at ZLC Wealth Inc. (ZLCWI), this is not an official publication of ZLCWI. The views (including any recommendations) expressed in this newsletter are those of the author alone, and are not necessarily those of ZLC Wealth Inc. The information contained in this newsletter is drawn from sources believed to be reliable, but the accuracy and completeness of the information is not guaranteed, nor in providing it does the author or ZLCWI assume any liability. This information is not to be construed as investment advice. Your own circumstances have been considered properly and that action is taken on the latest available information. This newsletter is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This information is given as of the date appearing on this newsletter, and neither the author nor ZLCWI assume any obligation to update the information or advise on further developments relating to information provided herein. This newsletter is intended for distribution in those jurisdictions where both the author and ZLCWI are registered to do business. Any distribution or dissemination of this newsletter in any other jurisdictions is prohibited. The rate of return shown is used only to illustrate the effects of the compound growth rate and is not intended to reflect future values of the Fund or returns on investment in the Fund. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the offering memorandum or prospectus of the Fund before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Performance results are not guaranteed, values may change frequently, and past performance may not be repeated.

IMPORTANT INFORMATION: The above commentary may contain an update on certain funds offered through ZLC Wealth Inc. Returns are net of fees and include reinvested dividends. The performance of the fund presented in this document may be for a different series of fund than the series that you hold in your account. The performance of the series that you hold may be different than what is shown. This information does not constitute an offer or solicitation to anyone in any jurisdiction in which such an offer or solicitation is not authorized, or to any person to whom it is unlawful to make such an offer or solicitation. These products may not be appropriate for all investors. Important information about the funds is contained in the offering documents which should be read carefully before investing. You can obtain these documents from ZLC Wealth Inc. Please speak to a ZLC Wealth Portfolio Manager or Representative to determine if these products are right for you.